Episode 17 – Fintech – All you wanted to know about Open Credit Enablement Network (OCEN) and what it means for businesses

Episode 17 – Fintech – All you wanted to know about Open Credit Enablement Network (OCEN) and what it means for businesses

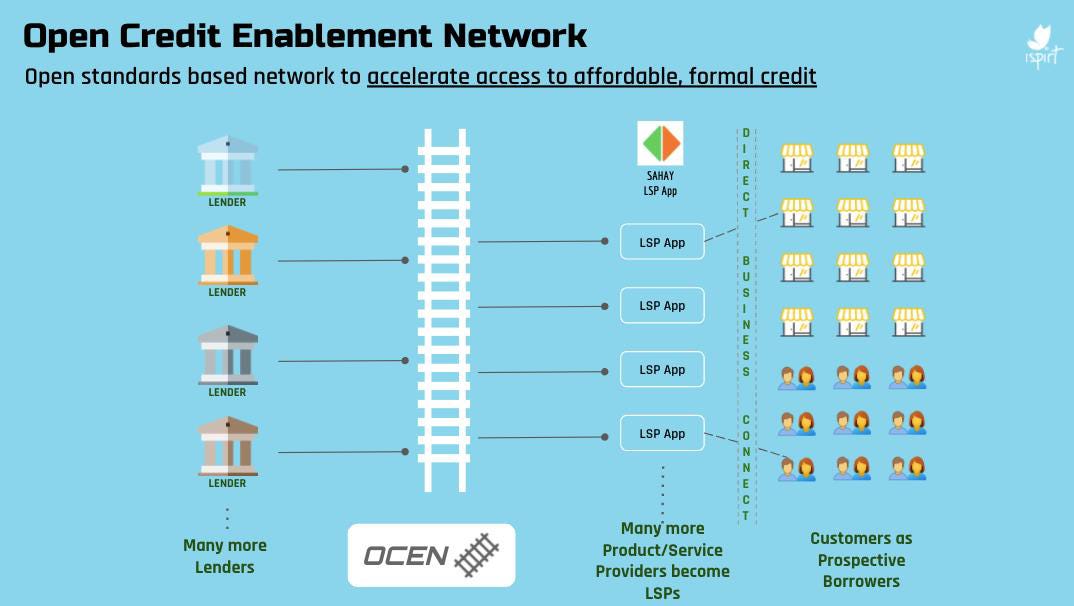

Simply put, OCEN is a framework of APIs for interaction between lenders, loan service providers (LSPs), and account aggregators.

IndiaStack has been facilitating Fintech growth in India since long. Its disruptive innovation offers open APIs as public digital infrastructure such as UPI, BharatPay, BBPS, Aadhar, AEPS, eKYC, eSign, DigiLocker, FASTag, and GSTN platform. Open Credit Enablement Network (OCEN) is the next chapter in the IndiaStack story. It is an initiative to unbundle lending and enable the creation of specialized entities, each specialized at one part of the job.

Simply put, OCEN is a framework of APIs for interaction between lenders, loan service providers (LSPs), and account aggregators. I previously did an explainer for account aggregators, which you can read here.

In this episode, I take a deeper look at OCEN and the possibilities with it.

Note – In case you are a fintech founder, looking to raise funds, I might be able to help. Reach out to abhishek@indiafintech.in. In case you are looking to invest in Indian Fintech, reach out. Would be happy to help. There are some amazing fintech players creating ecosystem plays and closing their rounds, with small allocations left. Great time to get in before they open up for larger, institutional rounds.

So, what exactly OCEN aims to do?

OCEN aims to create an ecosystem where any customer interfacing service provider (Amazon, Flipkart, cult.fit, Zomato, Swiggy, et al) can enable credit. It aims to provide a standard set of tools to participants of a typical lending value chain, allowing them to 'plug in' lending into their current operations.

This tech ecosystem is reimagining lending value chain aiming to have a Fintech-enabled market place by creating standardised building blocks. OCEN will enable access to lending ecosystem beyond traditional plays of banks and NBFCs.

OCEN ecosystem rests on four key pillars

Loan Service Providers (LSPs): Online intermediaries such as marketplaces, e-commerce entities, consumer platforms and digital businesses, which are close to end customers, are categorized as LSPs. These can embed credit products as part of their core offerings without having to significantly invest in technology or forming individual tie-ups with multiple lenders. Hence, they provide credit solutions to their customer base.

Borrowers: End borrowers, who will now be able to see credit options offered by multiple lenders on LSPs’ platform. Financing will gradually move from one-size-fits-all to ‘customized’ credit solutions, evaluated primarily on continuous cash flows rather than income and assets.

Technology Service Providers (TSPs): TSPs will be specialised entities offering innovative technology to help LSPs and lenders. A new set of opportunities will emerge for existing players, particularly within the Fintech segment.

OCEN framework

Source : Indiastack

There is a fourth pillar here as well – lenders. Effectively, Banks/NBFCs/small finance banks provide capital and access to core banking networks for the Embedded Finance Infrastructure company to build on.

So, what problem does OCEN solve for?

One of the biggest challenges in traditional lending models is the high cost of customer acquisition (including document verification, underwriting and collection framework), which makes it economically unviable below a certain threshold EMI, leaving a significant chunk out of credit potential– MSME credit gap of >35%.

Looking at the current MSME credit landscape, the overall debt demand is ~INR120tn; however, of this, 47% is non-addressable due to several factors (firms that have limited operational history, sick and redundant firms, or firms that voluntarily exclude themselves from formal financial services, etc).

The balance 53% is addressable, that is INR58tn can be served by FIs. Of this addressable demand, FIs address INR20tn. Thus, the total credit gap is estimated at INR38tn – 35% of overall demand.

Drilling further down, the contrast becomes even starker, wherein large part of credit off-take happens towards medium & large enterprise (>80% plus) and not so much on micro & small enterprises (sub 20%% levels). This largely is reflective of the challenges (essentially higher cost and effort) faced by traditional lenders in dealing with lower-size entities. This is essentially the gap which OCEN can broadly address.

Within lending landscape, while retail has seen significant growth over the past few years – and now is at INR77tn – forming 49% of credit. That said, personal loans still form sub-10% of the overall pie. More so, small-ticket personal loans (STPL) form only 6% of overall personal loans (and 60bps of overall retail segment). This could see significant traction with implementation of tech ecosystem.

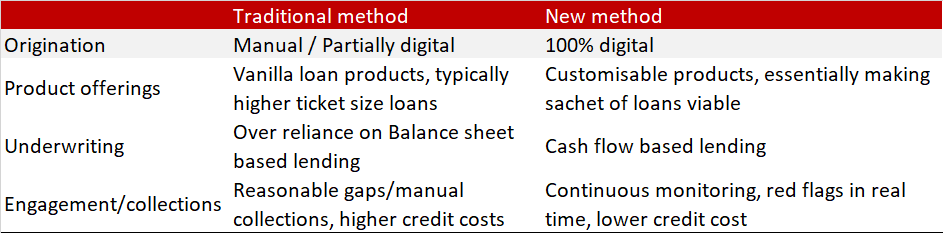

Lending landscape will undergo serious changes across all touch points

Source: Internet, Edelweiss, Abhishek Kumar

OCEN looks to be win-win for all involved in the credit ecosystem

This ecosystem addresses the concern, thereby pushing credit democratization. This is a win-win proposition for all stakeholders as it builds on system efficiency, thereby increasing profitability pool for all stakeholders. While nascent, building blocks being in place, reinforces confidence on scalability potential.

Ideally, these frameworks will end up promoting parity across the value chain–more access to data for players who were lacking it. Thus, Fintechs and new-age financiers will have wider opportunity bucket as data get democratised.

Moreover, looking at the current lending landscape, risk assessment for banks is generally more balance sheet oriented and with NBFCs more on cash flow-based lending. With the help of OCEN, banks will also be able to transition towards cash flow based risk assessment. On the other hand, NBFCs will have a larger part of transactional data, which till now rested with banks, and that in turn will strengthen lending models and even open up the funnel further.

Overall, for the three stakeholders, it’s a win-win –

Source: Abhishek Kumar

Who are the startups who are creating solutions on OCEN?

OCEN is a protocol. It is incumbent upon lenders and digital platforms to adopt these specs in the real world. That’s the gap between OCEN and financial inclusion in the real world.

Embedded Finance Providers fulfill that role. They provide the technology interfaces, modeling insights, and the advanced analytics that make innovative lending products a reality.

FinBox is one such Embedded Finance provider. Their solutions help develop a credit product configuration layer based on the customer demographics and data from the digital platform. As a result, they also boost conversions by enabling customized, in-context credit on the customer-facing platform.

So effectively, Embedded Finance companies help digital platforms and lenders come together and implement OCEN.

Here is what this implementation consists of:

Modifying the business processes and tech stack of digital lenders and digital platforms as per the OCEN protocol

Developing a digital acquisition channel with end-to-end loan application journey

Building FinTech partnerships with multiple lenders, platforms, credit enablement ecosystem (eNACH, PAN verification etc)

Writing cash flow-based and alternative data-based underwriting models

Developing analytics and business rules layer in collaboration with both parties

Developing a borrower communication and servicing layer in collaboration with both parties

Developing a payment reconciliation layer

Combining their financial know-how and tech expertise, Embedded Finance Providers leverage their unique position and digitize the lending lifecycle. They empower platforms to embed financial services within themselves and thereby unleash the real potential of OCEN.

Niro, another Fintech startup, plans to disrupt India’s consumer lending landscape by making embedded consumer credit products easily accessible to the country’s 624 million internet users.

Opportunities will emerge across value chain for founders who are nimble to catch this

In terms of ecosystem, I see services getting disintermediated and many ecosystem players jumping on board to tap into opportunities across the value chain. To elucidate, TSPs derived data providers, bureaus, underwriting modulers, and account aggregators will all have opportunities for new fintech players.

Riding UPI, we saw emergence of PhonePe, GooglePay, and Whatsapp Pay, among others, which changed the payments landscape. I expect similar ecosystem development to play through with the emergence of OCEN.

Hirings in Fintech Industry

Xpresslane is looking to hire a Sales and Marketing Head. Super interesting role with good equity on offer. Reach out to me on Abhishek@indiafintech.in and I will connect with the founders.

Antrepriz is looking to hire a Growth head. Reach out to me and will connect with the right person.

Finovate is looking for program managers in CEO’s office. Do reach out if you are interested

Kudos is hiring for a business analyst and a graphic designer. Reach out to either me or the founder, Pavitra here.

Latest happenings in the Fintech Industry

Niro, Embedded finance startup, which plans to disrupt consumer lending, raised $3.5 mn from Elevar and others.

AuthBridge, India’s largest Authentication player has raised Series A investment from an Infinity Alternatives led investor group.