Episode 19 – Fintech – Embedded Finance and the Fintech Future

Episode 19 – Fintech – Embedded Finance and the Fintech Future

The future is embedded and it's not just BNPL or credit products

Embedded finance is one of the topics which does come up in almost every conversation that I have with founders or investor. Or anyone associated, in general, with the fintech ecosystem.

In this episode, I take a deep dive on the What of Embedded finance, list down some of the players in India who are creating fantastic products and also talk about the future of embedded finance. Hop on!

Note – In case you are a fintech founder, looking to raise funds, I might be able to help. Reach out to abhishek@indiafintech.in. In case you are looking to invest in Indian Fintech, reach out. Would be happy to help. There are some amazing fintech players creating ecosystem plays and closing their rounds, with small allocations left. Great time to get in before they open up for larger, institutional rounds.

So what is Embedded Finance?

Embedded Finance or embedded banking is the seamless integration of financial services into a traditionally non-financial platform – think of Amazon Pay or Swiggy offering BNPL services to it’s customers and so on. It enables customers to access financial services within the app and in-context. For example, customers can make cashless payments within a food ordering app or a taxi service app. Embedded Finance enables businesses in the MSME, B2C, and B2B segments to increase their customer lifetime value, monetize their customer base, and vertically scale their product offering. It’s a potentially 7+ trillion dollar market as per Bain Capital!

Until recently, if a business wanted to offer financial services, they had to create a FinTech arm within their organization. This included significant expenditure, took years to build, and even longer to become profitable, if ever. Embedded Finance Infrastructure reduces the barrier (as per some claims, by upto 10x) for digital platforms to natively offer financial services to their customers. For the customer, Embedded Finance enables ‘native’ FinTech experiences inside the non-FinTech digital platforms which are closest to the customer.

Internationally, Stripe made headlines with its entrance into the banking world with Stripe Treasury in Dec’20. The news follows Google’s banking and payments announcement along with IPO bound companies such as Airbnb, DoorDash and Affirm all mentioning “financial services” in S-1 filings — a clear signal of how the sector will continue to stay red hot for the coming years.

What do all of these firms have in common? The subtle, almost passable, embedding of financial services. There has been an influx of new fintechs democratizing how to embed financial services across the spectrum, from investing, insurance, lending to banking (Think of Kudos or Karza Tech or Signzy or M2P Fintech). While many of these companies are in their nascent stages, they are achieving increasingly high valuations.

Why?

Because today, customers look for increasingly greater personalization and less friction while firms are looking for ways to improve monetization seamlessly. The ability to be at the right place at the right time, supporting consumers and merchants alike, where they want it, how they want it and when they want it — cannot be understated.

At the heart of embedded finance is the benefit of enabling any brand or merchant to rapidly, and at low cost, integrate innovative financial services into new propositions and customer experiences. To avoid developing noncore product additions in-house, companies will look to “building blocks” (or APIs) to take advantage of the big opportunity to extend customer lifetime value and address a wider variety of needs in one place.

This holds true for startups, digitally native brands and established brands, online and offline. For fledgling fintech startups or brands that want to provide financial services to their customers, working with APIs are often a no-brainer given the costs associated with building integrations in-house.

But imagine if you are a global ecommerce company and the benefit of not having to staff a know-your-customer compliance or fraud detection team. Or for lenders who can minimize risk and increase speed by not having to request a pay stub or personal information verification?

The end goal is to earn and build customer loyalty while generating new revenue streams (Think of Shopper’s Stop HDFC Credit Card or the one offered by MakeMyTrip). Historically, established brands have been served by banks with co-branded and “affinity” programs or partnerships. But this “offline” model is usually white-label or very “human-in-the-loop” with limited and inflexible capabilities. However, APIs can change this — a great example is Starbucks Rewards, heralded as a successful case of data, rewards and loyalty. No longer are brands just reselling leads, businesses can now directly participate in the product and distribution to improve margins.

Today, embedded finance is being used in a variety of ways: In the product (e.g., Tesla’s insurance offering), in distribution channels (e.g., a startup selling electronics insurance during their purchases), and in the technology layer (or building blocks) to improve the overall functionality (e.g., a lender leveraging a data API for instant underwriting).

Broadly, there are two separate building blocks into two buckets: providers (“plug and play” applications) and enablers (those that help financial services to be offered).

Providers include BNPL players such as LazyPay, Paytail, Earlysalary, ZestMoney, Simpl and more. Other providers include Lending players, wealthtech players, payments firms, Insurance and all other fintech services providers.

Enablers include fintech infrastructure firms such as Kudos Finance, Apollo Finvest, Karza Tech, Advance.ai, Hyperface, M2P Fintech and more. It also includes players operating in the open banking space such as Setu and those operating in the data security and connectivity space such as baffle and fize. M2P Fintech is another key player here which has been doing great things.

Broadly, there are 4 set of players in the embedded finance ecosystem –

Source : Abhishek Kumar, M2P Fintech

Solution providers

These players embed plug-and-play financial solutions onto online platforms increased focus on customer segments and loyalty. Usually, these are fintech firms that offer solutions tailored to the showcase platform/firms requirements. Their business models are typically pay-as-per-use, on-demand, and hybrid.

Data enablers

These are players who transport information back and forth between the solution providers and showcase platform. They use APIs, SDKs, and connectivity like BaaS as part of their technological infrastructure. They enhance or revamp an existing solution while BaaS providers rent out their core infrastructure to power the services.

Showcase platform

It can be a standalone site or a network where the solution is embedded and is accessible. It presents a frictionless buying experience to the end customer. The customers can access these platforms through the web, mobile, and POS. They create a link between the banks and consumers by providing end-to-end financial services.

Financial Institutions and other regulated bodies

These are banks, NBFCs, investment, and insurance entities, whose services are extended by the solution providers to the showcase platform. The core services of underwriting, risk management, regulatory compliance, and credit risks are taken up here.

All these players work together to unbundle and re-bundle financial services as per the business requirement and target customer segment.

Top considerations to embed with success

While the opportunity is clear, we are still in the early days and there are too many fractionalized solutions when aggregation is needed to scale and create longtail winners. In addition, banks won’t settle for becoming “dumb” finance pipes so don’t discount innovation out of incumbents. Case in point – IDFC bank!

We have witnessed the power of embedding materialize around the world. Just look at the massive success of superapps such as Singapore’s Grab or China’s WeChat or to a certain level SBI’s Yono, driving and improving usage and adoption with payments, banking, wealth management and insurance services.

Superapps have evolved their value by unifying disparate customer journeys — but this can only happen if information is in one place, programmable and accessible. While India has no superapp equivalent (yet), and embedded has taken longer with notable retreats from the likes of Uber Money, we’ll continue to see a shift to business models that embed financial services. But keep in mind that there are a number of ways to succeed with an even larger number of providers and enablers to choose from.

While existing financial technology has worked, there is lack of innovation and there is an opportunity to make the core services more functional and interoperable. Convenience has been one of the first major outcomes, but the future will have elements of UX consistency and brand uniformity so seamless that customers can’t tell it apart from the original product.

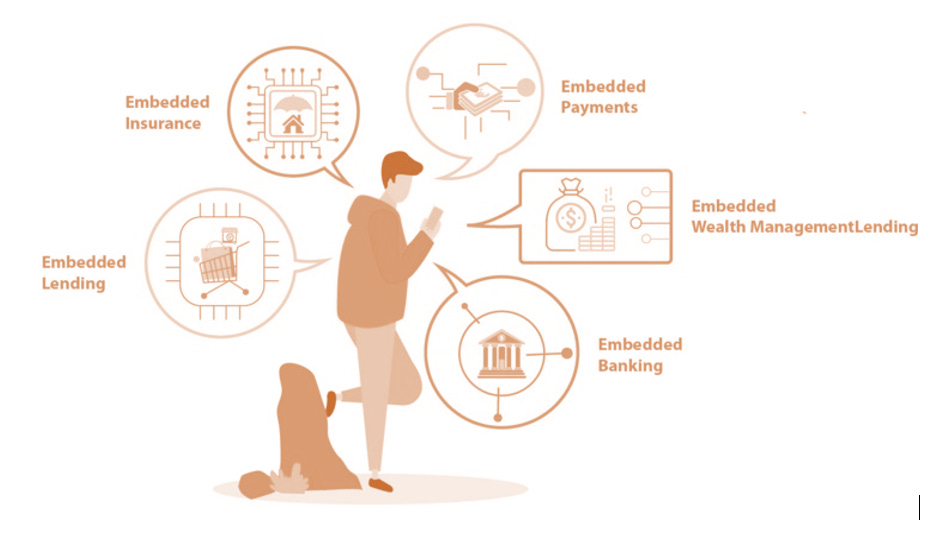

Also, while a lot of talk around embedded fintech is centered around credit products and payment, in essence it can embedded Insurance, embedded Banking, embedded Wealth Management to name a few. The opportunities are endless.

Source : Abhishek Kumar, M2P Fintech

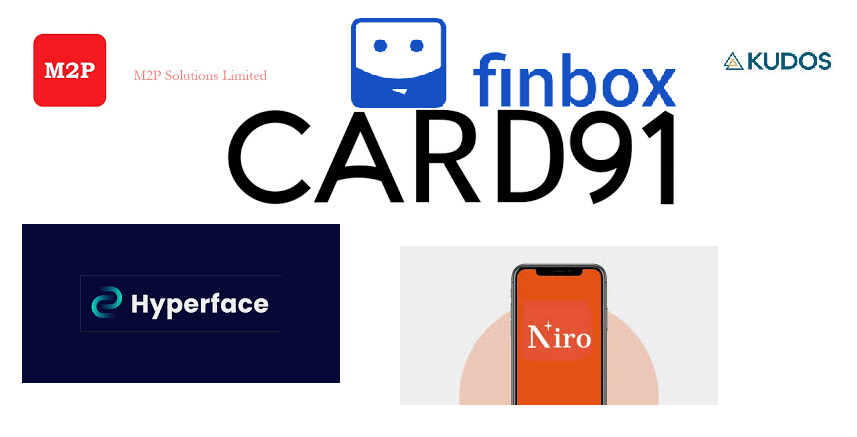

Who are the players in the Indian Embedded finance space?

Source: Abhishek Kumar

M2P Fintech is one of the global leaders in embedded financial infrastructure and act as a reliable tech layer between Banks, aspiring Fintechs and other Financial Institutions. They have been doing some exciting work in the space.

FinBox democratizes technology for FinTechs and Enterprises so that they can build financial services and products for the next billion Indians. They have been doing some great work in educating readers about embedded products as well.

Karza Tech is providing APIs for authentication and KYC services and counts almost all major BFSI player as its clients.

Niro, provides Lending as a Service Platform. It offers a solution that enables consumer platforms to provide financial services to the end customers. It also features a point-of-sale financing solution that enables retailers to provide financing options to the end customers. It uses APIs and SDKs for integrations.

Card91 provides open banking API solutions for payments & financial institutions. It offers plug & play infrastructure for issuing, controlling, viewing, and approving payments. It enables payment use cases via card issuance & management.

Hyperface Technologies provides credit card issuance solution for fintech and e-commerce firms. It provides APIs and SDKs to launch credit cards. It also provides credit card-as-a-service for fintechs for KYC management, real-time rewards, compliance & risk management, and more.

Earlier, I wrote an article on fintech infra firms providing lending as a service model – Click here to read the same!

There are many more fintechs getting into the space and I am, for one, excited by the developments here.

What are the expected benefits from embedded finance?

Benefits can be bucketed broadly into three stakeholders categories-

Benefits to merchants/vendors/platform players -

Increases in CLTV and other key business metrics - Platforms see a boost in their revenues through a boost in their Average Order Value (AOV), customer retention, and CLTV (Customer Lifetime Value).

Unlocks an alternate source of revenue - Platforms benefit from a revenue share while taking on none of the financial liability.

Increase in customer acquisition - Typically merchant-oriented businesses face very high acquisition costs. They provide expensive offers/incentives for the activation of the merchant on the platform. Adding credit is known to increase the activation of merchants on a platform in multiple ways.

Data led cross sell and upsell - Offering financial services unlocks valuable data about customers and their behavior which can be leveraged in interesting ways.

Benefits to financial institutions -

Access to large pools of customers - Financial institutions can access diverse borrower pools that have specific characteristics. They do so by leveraging the distribution capabilities of platforms (businesses) that have Embedded Finance. Example: A B2B E-Commerce platform (like Amazon) is connected with thousands of small businesses. Financial institutions can tap into this network by offering financial solutions to vendors on Amazon.

Build a more profitable business - Enhanced underwriting and efficient loan lifecycle management enable financial institutions to increase their margins and reduce costs for end customers.

Benefits to users -

Increased access to affordable financial services - Users get access to an array of flexible, easy, and cheaper financial services. They are approved for more financial services and on user-friendly terms.

Receive customized offerings - Users can avail tailored financial solutions that perfectly fit their requirements.

Improved customer experience - In-context financial service offerings improve users’ experience on the platform.

Thus, Embedded Finance brings together several parties and helps them to play to their strengths. The final combination is much greater than the sum of its parts!

So, what’s going to change?

One of the biggest impacts I see going forward is – A significant majority of fintech players will become acquisition channels for brands/platforms – Shopping as a Service will become prominent (Simpl has been moving in this direction). Specially for BNPL and Credit players, this will become a big revenue generator. I see BNPL becoming big and synonymous with embedded finance.

Vertical SaaS firms will become lenders and overall, I see SaaS players moving into fintech very significantly. This will also lead to improved revenues and hence, much improved unit economics for financial services.

So this is about it, for now. Do reach out to abhishek@indiafintech.in in case you want to discuss anything on fintech.

Hirings in Fintech

M2P Fintech is hiring for multiple positions, including a product manager. Reach out to Franklin for this role.

Xpresslane is looking to hire a Sales and Marketing Head. Super interesting role with good equity on offer. Reach out to me on Abhishek@indiafintech.in and I will connect with the founders.

Antrepriz is looking to hire a Growth head. Reach out to me and will connect with the right person.

Finovate is looking for program managers in CEO’s office. Do reach out if you are interested

Kudos is hiring for a business analyst and a graphic designer. Reach out to either me or the founder, Pavitra here.

Some interesting things happening in Fintech

Fintech startup Niro raised $3.5 million in a seed round led by Elevar Equity. The round also saw participation from multiple angel investors, including CRED's Kunal Shah, Bala Parthasarthy, Managing Partner at Prime Ventures, Nitin Gupta, and the Patni Family office, according to a statement shared by the firm.

M2P Fintech, which specialises in providing digital banking infrastructure to other fintech firms as well as banks, has raised $35 million in a Series C funding round led by Tiger Global at a post-money valuation of $335 million.

Zolve, a neobank enabling global access to financial services, today (27th Oct 2021) announced the closing of $40 million in Series A funding. The round was led by Partners of DST Global, who have previously led rounds in many prominent global fintechs such as Robinhood, Nubank, Chime, Revolut, and Wealthsimple. The round also recorded participation from Tiger Global, another prolific investor in the global fintech space, counting multiple unicorns in its portfolio. Alkeon Capital, as well as existing investors Accel and Lightspeed Venture Partners, also participated in the round.

Chennai-based fintech solutions company Hypto has raised $3 Mn in a seed funding round led by Stellaris Venture Partners. 3one4 Capital and Core 91 also participated in the round along with angel investors like Amrish Rau (CEO, Pine Labs) and Jitendra Gupta (CEO, Jupiter).