Episode 4 – Fintech – Comprehensive intro to India’s Insurtech Landscape

Episode 4 – Fintech – Comprehensive intro to India’s Insurtech Landscape

The sector has seen 2 unicorns (PolicyBazar and Digit) and a plethora of soonicorns and minicorns. A simple search shows up 360+ insurtech companies in India, 125+ of which are funded at various stage

Insurtech is one of the most talked about sub-segments. It’s the technology that lies behind the creation, distribution and administration of insurance business. Smartphone apps, wearables, claims processing tools, online policy handling and automated processing are all Insurtech. Insurtech is useful for collecting and analysing customer data to provide a better service ranging from ease of insurance product access to buying insurance to claims on the customer side and getting access to useful data to better underwrite, speedy customer acquisition and supporting agents for the whole customer journey and avoiding frauds on the insurance providers side.

The sector has seen 2 unicorns (PolicyBazar and Digit) and a plethora of soonicorns and minicorns. A simple search shows up 360+ Insurtech companies in India, 125+ of which are funded at various stages. Interesting times ahead in the space.

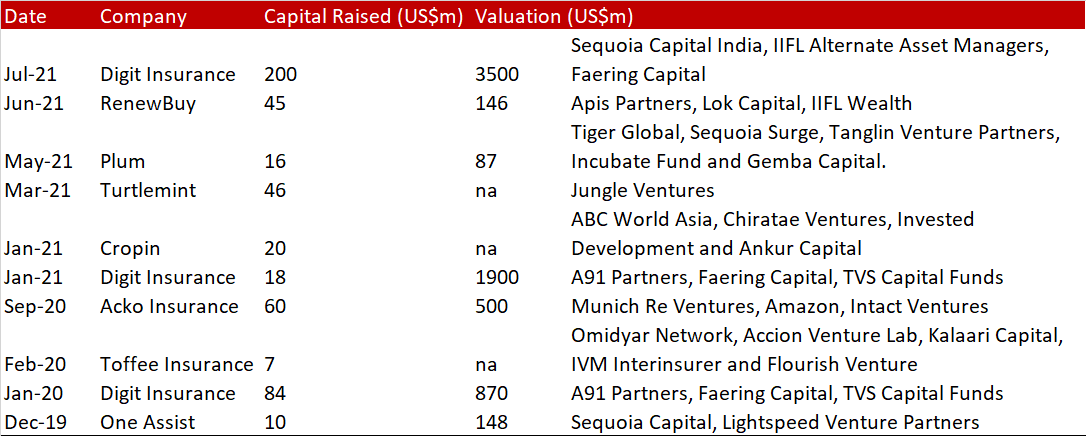

Indian Insurtech firms raised only US$11mn in 2016 but have raised ~US$350mn so far in 2021. In the past two years, funding has also become broad-based with manufacturers (Acko, Digit), PoSP/Brokers (RenewBuy, Turtlemint), and other niche players (Toffee, Cropin) attracting investor interest. Valuations are expanding – e.g. Digit's value has risen ~80% from US$1.9bn in Jan '21 to US$3.5bn in Jun '21.

Recent Transactions in the Insurtech space

Source: Abhishek Kumar

India Insurtech's consists of very meaningful sub segments which are large in themselves.

Web Aggregators: Most recognised vertical, with primary role as comparison portal and now wrapping underwriting, fulfilment, claims assistance etc. Key players include Policy X, ET Insure.

Analytics: Various providers of AI and data analytics are now focused on insurance. CropIn is a unique company here, powering agri analytics with a presence in 50+ countries. Arya AI, AskArvi, Pentation, Aureus, Mantra Labs are other players.

PoSP/Brokers: These players combine a tech platform (e.g., comparison platforms) with a network of offline agents. This helps to transform tied agents into open-market distributors. RenewBuy, Turtlemint, Gramcover, Coverfox are key players.

Sales/Claims facilitation: Insurtechs here focus on improving the sales & claims processes. Sureclaim specializes in health insurance claim advisory; LeadCRM & StickyNote simplify & improve agents' operations.

Micro/Contextual Insurance: Players here partner with primary insurers to develop unconventional products that are suited for a specific need/niche/ ticket size such as mobiles, cab rides, cycle, dengue, mobiles, even bags & pets. Key players are Toffee Insurance, OneAssist, Riskcovry.

Internet of Things (IoT): This segment creates a network of connected devices & service delivery to track consumer behavior & offer related services. GoQii and BeatO have built an ecosystem for health parameters while CarIQ focuses on motor IoT.

Health Ecosystem: Several healthtech companies are partnering with insurers to provide data analytics and policy cross-sell. 1mg, Pharmeasy, Practo are key health tech plays. Plum & Vital are focused on health insurance & ecosystem services.

Fintech Platforms: Players like PayTm and Phone Pe utilize their fintech platform to cross-sell insurance products

Key USPs of India Insurtech market – Complimentary rather than supplementary

Largely a partnership-driven approach. Unlike few sectors where tech startups tend to disrupt incumbents, insurtech ventures have emerged more as partners than disruptors of primary insurers. While Acko and Digit do compete with primary insurers, most insurtech companies help incumbents improve products and processes, expand the market and deepen penetration. For example, Web aggregators have helped to raise awareness, Toffee Insurance has helped tap into unique niches etc.

There are multiple ways in which tech ventures are collaborating with primary insurance companies to add value, some examples include: (i) Vymo helping SBI Life in lead conversions, (ii) Toffee Insurance collaborating with Bajaj Allianz in creating Dengue insurance, (iii) Cropin allying with primary crop insurers in assessing yield, crop failure probabilities and offering parametric insurance (iv) BeatO helping health insurers in diabetes cover with sharper data stack, (v) Gramcover providing last-mile access in onboarding rural customers, etc.

A little bit deeper breakdown of some of the interesting subsegments and companies within them would be interesting. Here’s a crack at the same

Micro / Contextual Insurance

One of the hottest sectors, several players are innovating to deliver bite-sized, contextual products to tap into multiple discrete niches. Toffee Insurance is a key player in this segment and has partnered with several primary non-life insurance players to offer innovative products like Cycle Insurance, Pet Insurance, Dengue Insurance, Backpack Insurance, Commute Insurance, etc. Toffee has a distribution reach of 4000+ point of sale outlets in 3000+ cities, with cycle insurance sold through 1000+ dealers. Similarly, Acko launched ride insurance in a tie-up with Ola where it insured 23 million rides in 10 months. Riskcovry, which is more of a platform for other firms, has also built an impressive niche product offering for: (a) nano retail biz, (b) startups, (iii) bill payment, (iv) renters, (v) bags and wallets etc. While micro insurance is an interesting way to address product/service gaps, many industry players believe that such insurers will have to pivot towards traditional products to attain critical mass.

OneAssist Consumer Solutions is a multi-service online insurance provider and offers app-based protection services on consumer electronic/electrical assets, such as the mobile phone, wallets, wearables, laptops. It also provides repair options for appliances like refrigerators, washing machines, televisions, and air conditioners on a warranty basis. In addition, the company deals in theft and damage insurance and offers facilities to pay credit card bills, along with monitoring them against fraud & misuse, hotel bill settlement, assistance for lost passports, etc. OneAssist has a presence in 400 cities with a customer base of 2mn+ and has serviced 180,000+ claims to date.

Founded in 2011 by Gagan Maini and Subrat Pani, One Assist has received total funding of US$42mn in 10 funding rounds, with the latest funding round being of US$9.52mn (Series C on Dec-19). In June 2017, the startup raised around $18 million (roughly INR 110 crore) in a round led by existing investor Sequoia Capital. The company had annual revenue of US$27.1mn (as on Dec-18) and was valued at US$148mn in Dec’19. Its key investors include Sequoia Capital, LightSpeed ventures, Moonstone Investments, Trifecta Capital, and Assurant Solutions – a US-based Fortune 500 Insurance provider. It is noteworthy, in our view, that Assurant’s investment into OneAssist is its first investment in India.

Riskcovry is a B2B2C platform that enables Banks, NBFCs, Fintechs, etc to offer digital insurance products to their end customers. Riskcovry offers its API and SaaS technology to enable insurance distribution business without the traditional overheads associated with building teams, tech, processes, getting license etc. Its platform is agnostic to insurer, product, channel, device and compliance license. Its clients include InMobi’s Glance, ZestMoney, Future Group’s Digital wallet FuturePay etc. The Company plans to sell close to 0.2m insurance products in FY22. It intends to quadruple its partner network within 15-18 months.

Founded in 2018 by Suvendu Prusty (Director & Principal officer), Vidya Sridharan (CTO), Sorabh Bhandari (Director) and Chiranth Patil (Director), Riskcovry has raised US$6.5m of funding to date. It counts Omidyar Network India, Pentathlon Ventures, DMI Sparkle Fund, Better Capital, Bharat Inclusion Seed Fund, and Varanium Capital among its investors.

Specializes in designing and selling contextual & unique microinsurance products including (i) cycle insurance, (ii) commute insurance, (iii) backpack insurance, (iv) dengue insurance, (v) pet insurance etc. It aims to sell insurance as a commodity rather than as a financial product by unbundling it.

They use behavioral and consumption data to co-create insurance products and possesses abilities aided by artificial intelligence, machine learning and a substantially wide distribution network of over 4000+ point of sale outlets across 300 plus cities. Cycle theft insurance forms a good part of its business and Toffee sells this product through a network of 1000+ cycle dealers across 120+ cities. The cycle insurance cost can go to as low as INR180 per year, which enables the company to tap into lower segments of the market. It has been distributing plans through API, SMS, mobile, whatsapp and the company has sold more than 0.2mn policies across 2,500+ cities with a claim settlement ratio of 99.1%.

Currently, Toffee Insurance partners with Hero Cycles, Wildcraft, Eko, and Apollo Hospitals and is backed by ICICI Prudential, Religare, HDFC Ergo, and Tata AIG Insurance among many others. It has distributed policies to >115,000 customers with more than 80% being first time buyers. It has tied up with several life/non-life insurance providers such as HDFC Ergo, Indiafirst Life, Manipal Cigna, ICICI Pru Life, Tata AIG, Religare, Bajaj General etc.

Founded by Rohan Kumar (CEO) and Nishant Jain (CPO), the company has had 3 rounds of funding till Dec’19 having raised ~US$7.1mn in toto, with key investors being Omidyar Network, Accion Venture Lab, Kalaari Capital, IVM Interinsurer, Flourish Venture, among others. The company is still an early-stage venture with US$251k as annual revenues in CY19.

POSP/Brokers (Distribution)

Post IRDAI 2015 regulation on Point of Sales Persons (PoSP), several insurtech startups have built hybrid distribution model by bringing together offline pool of sub-brokers (erstwhile agents) under one umbrella broker entity and combining that with backend digital/mobile app support to onboard and service customers. Turtlemint and RenewBuy are the two most prominent names in this space and have undergone multiple rounds of funding. Turtlemint has onboarded 100,000+ advisors (vs. just 7000 in 2017) and aims to take it to 340k+ 2025. It had premium of US$167mn in FY17 and claims to be on track to achieve US$2bn by FY25. 60% of its business came from B30 locations. Renewbuy has more than 35,000 sub-brokers on its platform that service >2.7million customers and more than 100k+ transactions a month. Renewbuy had posted 40% growth in revenues in 1HFY21- a period when the general insurance industry saw a sharp decline.

Insurance Analytics

Insurance offers wide scope to use big data and AI-driven data analytics. Within this space, CropIn has carved a unique niche and is a full-stack AgTech company that processes farm-related information by combining machine learning, satellite monitoring, and weather analytics. Cropin’s effectiveness has also helped it to branch out into multiple countries. It has so far digitized more than 13 million acres of farmland, touching the lives of nearly 4 million farmers across 52 countries. Its risk platform has processed 160 MN Ha of land area, and has the potential to impact 70 million farmers globally in the next 3-5 years. There are multiple other AI-driven analytics ventures such as Arya AI. Mantra Labs, Pentation Analytics, etc that help insurance companies in process automation that helps speed up and improve underwriting, client acquisition, claims management, compliance, agency management, fraud prevention, prediction and detection, etc.

Some other interesting firms in the space

ClaimBuddy is the first medical claim support company in India to offer its users assistance in hospital selection, help in calculating treatment costs, claim assistance, access to home care, diagnostic test booking, and hassle-free appointment bookingacross 35k+ doctors. ClaimBuddy has medical claim specialists who evaluate customers' medical insurance to help resolve their queries/provide assistance.

A hybrid insurtech venture that aims to tap into the virtues of both online and offline modes of distribution. It works with more than 0.1m advisors, equipping them with digital tools to offer wider and relevant products. It has been partnering with insurance advisors across India. Its platform supports its advisors through tools like a mobile CRM, a repository of video content for customer education, and social media marketing features. Turtlemint also has an online education product with a wide range of courses on financial products, advice-based sales techniques, and other soft skills – 20,000+ learners are active on it on a monthly basis. It has also launched a webaggregator platform for retail insurance for life and non-life products (auto and health).

It has partnered with 40+ insurers and serves more than 1.5m customers. It offers products across both life and non-life insurance with a focus on microentrepreneurs and the rising middle class. Within life, it offers both protection and savings products, and within Non-Life, it is focussed more on health and motor insurance. Advisors play a critical role in bridging the gap in tier 2 and 3 cities and towns.

It was founded in 2015 by Anand Prabhudesai & Dhirendra Mahyavanshi. Mr Prabhudesai has ~15 years of experience at Corporates including Yahoo, Nokia and Quickr. Mr Mahyavanshi has ~13 years of experience, primarily at ICICI Lombard and Quickr.

GoQii is a cloud-based IoT ecosystem providing a comprehensive preventive healthcare toolkit to individual and corporate customers. Its ecosystem of services includes a fitness tracker, a mobile app, preventive and curative counselling/consultation with Doctors/Experts/Fitness Coaches, access to unlimited cloud storage for personal health records, tie-ups with diagnostics centers. It has tied up with Thyrocare to help users directly book tests with the lab and access results on the app. It also helps users to construct diet plans and nutritional/medicinal regimens for effective healthcare. GoQii relies extensively on data and analytics and has the potential to facilitate sharper pricing and claims management to health insurance companies.

The company was founded in 2014 by Vishal Gondal (CEO), Abhishek Sharma (COO), Sachin Janghel (CTO) & Champ Alreja (CBO). It counts Mitsui, NEA, Megadelta, DSG Consumer Partners, Galaxy Digital, Denlow Investment Trust, Edelweiss, Cheetah Mobile, GWC, Ratan Tata and Vijay Shekhar Sharma among its investors, having raised ~US$50m in capital to date.

Given all of this, what is clear is that the biggest winners here seem to be the incumbents!

While several insurtechs are carving out niches for themselves across the value chain, most primary insurers are also focusing on boosting their captive digital capabilities and helping incubate new startups. Given the proactive approach of incumbents, we see limited scope for insurtech startups to materially disrupt their biz model. Companies like IPRU Life, HDFC Life, ICICI Lombard, SBI Life, Max Life, Bajaj Allianz, etc, are sitting on deep customer connections, won over decades of hard work in customer servicing.

Hence, it will likely be difficult for startups to materially upend existing businesses. However, there is significant scope for symbiotic partnerships between insurers and insurtechs to address inefficiencies and white spaces to improve products, processes, & pricing and expand the market.

I will dive deeper down on this specific space in my next episode – Watch out!

Closing thoughts on Insurtech

Given the symbiotic relationship amongst players, rising number of hybrid (phygital models) and rise of JAM like govt. platforms such as National Health Stack, the overall space is set to emerge out of the comparison/insurance seller model into deeper, data backed specific use case backed firms. A lot of them has been discussed in this episode and will keep doubling down on them!

Hirings in Fintech

Toffee Insurance is hiring for 15+ positions ranging from Product Designers, Product Managers, Content Writers and Tech team. You can reach out to Rohan or check out their Linkedin page for more

Riskcovry is hiring for product managers and developers. Connect with Sorabh, founder of Riskcovry

GoQii is hiring for product managers and software testers. Reach out to Vishal.

Latest news in Fintech

Agritech startup Farmers Fresh Zone raises Rs 6 Cr in pre-series A round led by IAN